Showing posts with label production. Show all posts

Showing posts with label production. Show all posts

07 March 2012

Read more... Sphere: Related Content

14 January 2012

Will New Zealand be the first developed country to evolve a steady-state economy?

New Zealand will inevitably make a transition to a steady-state economy. The onset of energy descent — having less and less energy to use with each passing decade — will push it to do so sooner rather than later. The critical question is whether the transition to a steady-state economy will be by design or disaster

by Jack Santa Barbara | Jan 11 2012 by Feasta in Energy Bulletin | Jan 13 2012

Read more... Sphere: Related ContentEnergy Resources Saudi oil output 'stretched to the limit'

Saudi Arabia, the world's leading oil exporter, has for decades used spare production capacity to cover shortfalls in output by other oil states and prevent prices spiraling in times of crisis

United Press International | Jan. 13, 2012

Read more... Sphere: Related Content11 January 2012

Warm and Fuzzy on Geothermal?

The Earth started its existence as a red-hot rock, and has been cooling ever since. It’s still quite toasty in the core, and will remain so for billions of years, yet. Cooling implies a flow of heat, and where heat flows, the possibility exists of capturing useful energy

Tom Murphy | Do the Math | January 10, 2012

Read more... Sphere: Related Content

Geysers and volcanoes are obvious manifestations of geothermal energy, but what role can it play toward satisfying our current global demand? Following the recent theme of Do the Math, we will put geothermal in one of three boxes labeled abundant, potent, or niche (puny). Have any guesses?

03 January 2012

Indonesia takes steps to increase rice production amid climate change

Indonesia is taking steps to increase rice production amid ongoing climate change, Agriculture Minister Suswono said here on Monday

Xinhua | Jan. 2, 2012

Read more... Sphere: Related Content20 December 2011

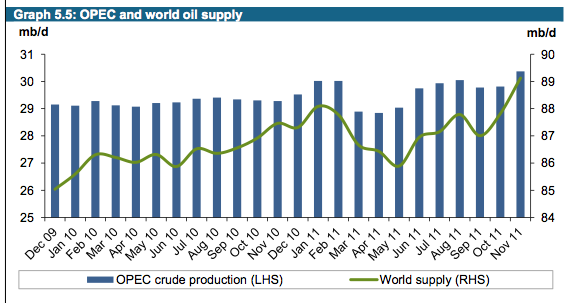

OPEC says, 'Don't count on us' for more supply

The results of OPEC’s latest meeting to set oil production quotas were announced this morning. Instead of production targets for individual countries, a group production ceiling of 30 million barrels a day was set. This amount is a bit less than OPEC produced in November 2011 (actual 30.367 mbd), according to its reckoning, and less than it would have produced most of 2011, if Libyan production had stayed on line, based on the amounts shown in its November Oil Market Report

by Gail Tverberg | ASPO-USA's December 19th Newsletter in Energy Bulletin | Dec 19, 2011

Read more... Sphere: Related Content

Figure 1. Recent oil production for World and for OPEC, according to OPEC November Oil Market Report.

25 March 2010

China overtakes US in green investment: study

China has surpassed the United States as the top investor in clean energy with the rising Asian power becoming a "powerhouse" in the emerging field, a study by environmentalists said

Shaun Tandon | AFP in Yahoo! News | 24 March 2010

Chinese investment in clean energy soared by more than 50 percent in 2009 to reach …More

The report said that China has shown determination to be on the frontline of green technology, while US investors have been put off by uncertainties amid the legislative battle on climate change.

Chinese investment in clean energy soared by more than 50 percent in 2009 to reach 34.6 billion dollars, far more than any other country in the Group of 20 major economies, the study led by the Pew Charitable Trusts said.

Total US investment was about half that at 18.6 billion dollars, the first time in five years that the world's largest economy lost the top spot in clean energy, the study said.

"China is emerging as the world's clean energy powerhouse," Phyllis Cuttino, global warming campaign director of the Pew EnvironmentGroup, told reporters on a conference call.

"This represents a dramatic growth when you consider that just five years ago their investment totaled 2.5 billion dollars," she said.

China has also overtaken the United States as the top emitter of carbon blamed for global warming and came under fire for its role in December's much-criticized UN climate summit in Copenhagen.

But the study found that China had made a strategic decision to invest in wind and solar technologies as it copes with sharply rising demand for energy -- and has set some of the world's most ambitious targets on renewable energy.

The study also found strong investment by Britain, which ranked third with 11.2 billion dollars for clean energy; Spain, which came in first in green investment when taken as percentage of gross domestic product, and Germany.

Nations seen as struggling in the clean energy competition include the United States, Australia and Japan, the study said. Cuttino said the three nations have "less consistent, clear and long-term policies in place."

US President Barack Obama, Australian Prime Minister Kevin Rudd and Japanese Prime Minister Yukio Hatoyama have all championed climate action but none of the countries have set in motion nationwide plans to curb emissions.

But the study noted that Australia had potential in wind energy and said Japan was "one of the G-20's most promising growth markets" if the resource-poor nation carries out plans to ramp up solar and wind power.

The study found that even though the United States dominates technological innovation, its investment in clean energy tumbled 42 percent last year from 2008 levels.

The researchers partly blamed the global economic slowdown but also said there was a lack of direction. Climate legislation has been stalled in the Senate, although Obama allies have vowed to push it ahead now that Congress has completed the top priority of expanding health care.

John Woolard, chief executive officer of California-based solar plant builder BrightSource EnergyInc., said that the government needed to take action to create markets.

"We have never had certainty or predictability in the United States," Woolard said. "We have not had a thoughtful and coherent energy policy in this country for decades."

Obama and his congressional allies argue that curbing emissions will open up a new green economy, helping fuel the economic recovery.

Many Republican leaders are skeptical, saying that restrictions on carbon would only worsen a fragile economy.

Copyright © 2010 AFP

Copyright © 2010 Yahoo! All rights reserved

Read more... Sphere: Related Content22 March 2010

Energy minister will hold summit to calm rising fears over peak oil

Lord Hunt calls UK industrialists together to discuss government response to any early onset of decline in global oil production

guardian.co.uk | 21 March 2010

A report last month warned of complacency over the huge dislocation from a terminal decline in global oil production. Photograph: David McNew/Getty Images

Lord Hunt, the energy minister, is to meet industrialists in London tomorrow in a bid to calm mounting fears about the disruption that could follow a sudden shortage of oil supplies.

In a significant policy shift, the government has agreed to undertake more work on whether the UK needs to take action to avoid the massive dislocation that could be caused by the early onset of "peak oil" – the point that marks the start of terminal decline in global oil production.

Jeremy Leggett, the executive chairman of the renewable power company Solar Century and a leading figure in the UK industry taskforce on peak oil and energy security, said the meeting, to be held at the Energy Institute, showed a welcome new sense of urgency.

"Government has gone from the BP position – '40 years of supply left, the price mechanism works, no need to worry' – to 'crikey'," he said. "BP and others are telling us that, but you lot, Virgin, Scottish and Southern, and others are telling us something completely different. We do not know who to believe. Let's do a proper risk assessment with industry," he said.

The meeting is expected to include executives from the taskforce members including Virgin, Arap, Stagecoach, Scottish and Southern Energy, and Solar Century as well as other industrialists.

The decision to hold the talks came after the UK industry taskforce on peak oil and energy security last month issued a provocative report, The Oil Crunch: a Wake-up Call for the UK Economy, in which it warned of the dangers of complacency.

Sir Richard Branson, founder of the Virgin Group, whose rail, airline and travel companies are sensitive to energy prices, warned then that the coming crisis could surpass the credit crunch. "The next five years will see us face another crunch: the oil crunch. This time, we do have the chance to prepare. The challenge is to use that time well," he said.

The government had previously played down the risks arising from peak oil after the Wicks review in the summer in effect dismissed the idea that global demand for oil could soon outstrip supply.

A spokeswoman for the Department of Energy and Climate Change confirmed last night that Hunt and a range of energy-policy civil servants would be holding "private and behind-doors" talks at the Energy Institute. But she played down the significance of the session, saying the government had always taken supply issues seriously and met different parts of industry on a regular basis. "We do this all the time; it is just a normal stakeholder meeting," she insisted, adding that there was no "marked" change in ministerial policy.

The issue of peak oil arose last November when whistleblowers inside the International Energy Agency alleged the problem had been deliberately downplayed over a long period. BP and other oil companies insist that there is little danger of the world running out of oil because new areas such as Brazil, and more recently Uganda, are always opening up to development. BP chief executive, Tony Hayward, believes demand will fall as prices move up., pushing back any major peak-oil dislocation.

But booming demand in China, India and the Middle East has pushed up the price of crude to more than $80 a barrel and UK petrol prices are close to record levels.

Amrita Sen, an oil analyst at Barclays Capital, believes the price of crude could pass $100 this year and reach nearly $140 by 2015. Francisco Blanch, of Bank of America Merrill Lynch, has speculated it could hit $150 within four years.

Leggett says all these scenarios could be much too optimistic. He is convinced that Britain must prepare as quickly as possible for a situation when oil becomes so expensive that international trade is hampered and globalisation breaks down.

Peak oil used to be the preoccupation of a small minority, but a parliamentary group has been set up to follow the issue and an increasing number of industrialists have begun to worry about it.

Ian Marchant, Scottish and Southern Energy's chief executive, is one who now believes global demand for oil is on the brink of outstripping the ability to produce it. At the launch of the Oil Crunch report, he said: "The west has been far too profligate in its use of oil and the price is going to say: stop it now and start using your oil as a scarce commodity."

guardian.co.uk © Guardian News and Media Limited 2010

Read more... Sphere: Related Content21 March 2010

The net energy of pre-industrial agriculture

Following on from yesterday's discussion, I want to make a point that seems like it must have been made before, but I cannot quickly find a good discussion of it. That is that the net energy of pre-industrial agriculture, taken as a whole energy-gathering system, must have been low, with EROEI probably on the order of 1.1-1.6 depending on place and time

by Stuart Staniford | Early Warning in Energy Bulletin | Mar 20 2010

Prior to the industrial revolution, the main source of primary energy in society was biological - agriculture and forestry, with a significant assist from water mills. The biological energy was used to feed horses (used themselves in ploughing, but also in transportation), as well as agricultural workers. The water-mills were primarily used to mill flour (ie also used in agricultural production, for the most part).

My point is the following - we know that the vast bulk of the pre-industrial population were involved full-time in agricultural production, and so were essentially part of the input energy (they, and their horses, had to be fed in order to go out and till the ground, harvest the crops, etc). Thus, most of the population was essential to the operation of the energy gathering system, and not part of the surplus generated by that system. Peasants by and large had pretty close to the minimum in terms of housing, furnishings, and clothing, and children and the elderly can probably be assumed to be involved in household economies to the extent they were capable. There were basically three places where an energy surplus generated by medieval agriculture could go:

- Population growth

- The church

- Goods and services consumed by the rich, the middle class, and the military

Now, the first, population growth, was not very different from zero. Here, and in most of the rest of the discussion, I am going to rely heavily on Braudel's classic three volume study Civilization and Capitalism, 15th-18th Century, particularly the first volume, The Structures of Everyday Life. On p46, he gives estimates of annual population growth in Europe as follows - 0.62% between 1600 and 1650, 0.24% between 1650 and 1750, and 0.4% between 1750 and 1800, and 0.46%. Ie consistently less than 1%. Given that society was mostly fed on annual crops, in EROEI terms, this means that an EROEI of less than 1.01 would be required to explain population growth, and we can essentially neglect it compared to the other terms in the surplus.

The second factor, the church, we can bound because we know that the church was generally supported by a tithe, in which 10% of food production and craft goods had to be turned over to the church. Now, some of this tithe was used for relief of the poor and hungry, and thus wasn't really surplus. You could also argue that the religious functions of the church were actually necessary for the operation of pre-industrial society, and so weren't surplus on those grounds. Also, I would guess that collection of the tithe was imperfect. But for the purpose of establishing an upper bound, let's treat it that the church was entirely surplus to agricultural production and that the tithe was all collected. Thus we need an EROEI of at most 1/0.9 = 1.11 in order to support the church as a surplus. Let's call it 1.1 as a rough number.

The last factor, goods, housing, etc consumed by the non-peasantry is the hardest to estimate. However, I argue that it must have been roughly bounded by the fraction of the population that lived in towns rather than in small villages and on isolated farms. It's a reasonable assumption that the population of villages was for the most part either directly involved in agricultural labor, or in the production of goods and services immediately required in agriculture (the village blacksmith, the miller, etc).

Now, probably, the population of the towns were somewhat involved in good and services utilized in agriculture also (eg a central function of towns has always been to provide markets to allow trade in goods to occur in the surrounding countryside, and between regions). Still, it's probably a reasonable assumption that non-agricultural production was primarily centered in the town - armorers, furniture makers, masons, etc. And it's probably also a reasonable assumption that the ratio of horses to people was not markedly higher in the town than in the country given that horses were directly used for ploughing and also for transportation of agricultural goods. In any case, only about a third of crop production was fed to horses, so it wouldn't devastate my case if this last assumption was somewhat wrong. Given these assumptions, the energy consumption of town versus country will approximately scale with population - it's unlikely town dwellers ate vastly more than country dwellers - not more than 10-20% more or they would all have been grossly obese (it seems unlikely that town dwellers engaged in more physical labor than country peasants, so surplus food consumption would have gone to fat).

Now, historians have attempted to estimate the fraction of the population living in towns at various times and places. Braudel (p483-484) summarizes the situation as follows ([] insertions are my clarifications):

Recent calculations by Marcel Reinhardt conclude that in France in Cantillon's time [the early 1700s], the urban population was only 16% of the total. And, of course, it all depends on the base level adopted. If towns are considered to be settlements of over 400 inhabitants, then 10% of the English population was living in towns in 1500, and 25% in 1700. But if 5000 is taken as the minimum definition, the figure would only be 13% in 1700, 16% in 1750, 25% in 1801. It is therefore evident that all the calculations would have to be repeated using identical criteria, before one could make a valid comparison of the degree of urbanization of the different regions of Europe. At present, all we can do is identify certain particularly low or high levels.

At the bottom of the scale, the lowest urbanization figures relate to Russia (2.5% in 1630; 3% in 1724; 4% in 1795, 13% in 1897). So the figures of 10% for Germany in 1500 is not insignificant compared to the Russian figures. The same percentage is found in colonial America in 1700, when Boston had 7000 inhabitants, Philadelphia 4000, Newport 2600, Charlestown 1100 and New York 3900. And yet, in 1642, in New York (still known as New Amsterdam) 'modern' Dutch brick was already replacing wood in house-building, a clear sign of growing prosperity. The urban character of these centres where the population was still of modest size is clear to see. In 1690 they represented the degree of urban tension permitted by a total population of 200,000 or so, scattered over a vast area: about 9% of the whole. In about 1750, of the already dense population of Japan (26 million) 22% were already living in towns.

(He then goes on to discuss the somewhat higher urbanization in 16th-18th century Holland, but I am going to discount that example because Holland was a small country that was already a major trading hub for all of Europe, and so I don't think can be taken as a reasonable sample).

Thus we see figures ranging from about 3% urban population (in Russia) to 20-25% in late pre-industrial England and Japan.

Expressed as EROEI then, and including the 10% church term, we get a range from 1/(1-0.1-0.03) = 1.15 in Russia to 1/(1-0.1-0.25) = 1.54 in England and Japan shortly before the industrial revolution. Since we certainly don't have three significant figures of precision here, let's call it 1.1 to 1.6. Note that, to the extent the church tithe was not surplus, and town economic production was actually required for agriculture, these estimates are probably upper bounds (with some possibility of slightly higher numbers if animal energy usage was higher in towns than I am assuming, or if agricultural peasant households actually had some consumption of goods that could reasonably be considered surplus).

So it's against this backround that one need to consider the introduction of fossil fuels, and their possible replacement now with other forms of energy.

It's also clear that modern biofuel EROEI's are in the same range as pre-industrial agriculture, and therefore are completely unsuited to support an industrial civilization.

~~~~~~~~~~~~~~~ Editorial Notes ~~~~~~~~~~~~~~~~~~~

Read more... Sphere: Related ContentAlthough it is not relevant to Stuart's general point, the question of how the surplus was divided was very important to the vast majority who worked the land. It made the difference between misery and a satisfying if modest existence. Consequently pre-industrial history is rife with struggles over taxes, tithes, access to the commons, etc. -BA

14 March 2010

Journey to the Center of the Earth

Miles below the ocean floor lies enough oil to power the U.S. for more than a decade—and perhaps our best shot at energy independence

By Matthew Philips | NEWSWEEK | Mar 12, 2010

From the window of a helicopter 1,500 feet above the Gulf of Mexico, oil platforms look like Tinkertoys in a swimming pool. Dozens dot the horizon stretching south from New Orleans and continuing out as the water deepens and turns a darker blue. Then, about 50 miles offshore, the platforms stop, and for the next hundred miles there's nothing. This is the deepwater Gulf of Mexico, where the ocean floor is 8,000 feet down and covered in a heavy layer of muck. Below that is an ancient salt bed several miles thick, and hidden under that, trapped tens of thousands of feet down, there's oil—billions and billions of barrels of it. And it's all in U.S. waters.

Chevron's Tahiti platform, about 190 miles offshore, first appears as a speck in open water. Even up close, its size is deceiving. A three-level structure sits above the surface, but its 555-foot hull is entirely submerged. At 714 feet tall and weighing more than 80 million pounds, Tahiti is the equivalent of a 70-story skyscraper floating in 4,000 feet of water. The first thing you notice when stepping onto its platform is a high-pitched hum: the sound of thousands of barrels of oil being pulled from the depths and pumped back to shore.

To Chevron, it's among the most beautiful sounds in the world, proof that a decade of investment in deepwater-drilling technology is beginning to pay off for big oil companies like itself, as well as BP, ExxonMobil, and Shell. After a string of hurricanes led to seven straight years of declining oil production in the Gulf of Mexico, a handful of new deepwater projects reversed the trend in 2009. This year deepwater oil is likely to power the first year-over-year increase in total U.S. domestic production since 1991. The turnaround comes as President Obama is making it a priority to wean America off foreign oil. That will require replacing more than half the oil we consume, or nearly 10 million barrels a day, even though domestic oil production has dropped 50 percent since 1970.

Oil producers like Chevron say offshore drilling represents our best shot at energy independence. Today some two thirds of U.S. production comes from land-based reserves, mostly in Texas and Alaska, but those sources aren't producing the way they once did. The U.S. government estimates that the Gulf of Mexico holds somewhere around 70 billion barrels of oil, 40 billion of which remain undiscovered in the deep water. Combined with the entire Outer Continental Shelf, there's thought to be more than 85 billion barrels of undiscovered crude off the coast of the U.S., more than a decade's worth of oil at our current pace. By 2020, 40 percent of U.S. oil could come from offshore, according to analysts at IHS Cambridge Energy Research Associates.

With easily accessible oil in decline around the globe, oil majors are vying for reserves hardly worth a second look a few years ago: plumbing the frigid waters off Greenland, where icebergs have to be towed away from rigs; sifting the viscous tar sands of Alberta, Canada; venturing into the rainforests of Venezuela's Orinoco Basin; and probing more than 4,000 feet below the ocean off the shores of Ghana. Last year Brazil's state-owned Petrobras drew the first oil from its 9.5 billion to 15 billion barrels of proven new reserves buried below 4.5 miles of sea, sand, rock, and salt, and spread over an area larger than Britain, 185 miles off the coast of Brazil.

In the U.S., however, offshore drilling remains politically fraught. Environmentalists argue that we can achieve energy independence by cutting demand and ramping up renewables. They add that the thousands of gallons of mud deepwater drilling unearths contain toxic metals—mercury, lead, and cadmium—that may end up in the seafood supply. The water that comes up from wells contains a toxic mix of benzene, arsenic, lead, and various radioactive pollutants, according to studies by the Natural Resources Defense Council. Storms only make things worse: hurricanes Rita and Katrina led to 125 spills from platforms and pipelines on the Outer Continental Shelf, releasing nearly 685,000 gallons of petroleum products into the ocean.

But since 9/11, the imperative to reduce our reliance on Middle Eastern oil appears to be trumping environmental concerns. Republicans have long been in favor of more drilling, and now Blue Dog Democrats like Virginia Sens. Mark Warner and Jim Webb are lobbying Interior Secretary Ken Salazar to make offshore drilling a priority. In a December 2009 Rasmussen poll, 68 percent of Americans supported offshore drilling in domestic waters.

So while the world debates capping carbon emissions, oil companies are busy plowing their billion-dollar profits back into deep water. The Gulf of Mexico is the front line of this effort, largely because it's one of the few places on earth where private companies are still allowed to operate. "In most places in the world, there's a growing consensus that oil assets should be run by the state," says Jeff Rubin, a former chief economist at CIBC World Markets. "The number of places where the private sector has the right to be is getting smaller every day."

Chevron's Tahiti began pumping its first oil in May 2009, making it the deepest-producing offshore oil platform in the world. It is already yielding 125,000 barrels a day and delivered more than $1 billion in revenue in its first five months of operation. Chevron and its partners spent $2.7 billion getting Tahiti to this point; this year the company will add up to six more wells.

The brainpower behind all this is back in Houston at Chevron's North American Exploration headquarters in the former Enron building. Geologist Barney Issen sits on the fifth floor in what's called the Viz room, where he manipulates 3-D computer models of the Tahiti field. The proprietary model represents millions of dollars and years of work for Chevron. It's the company's road map of the deepwater gulf; without it, Chevron would be groping in the dark down there.

It takes months to drill a deepwater well, and it can cost more than $100 million. Temperatures exceed 450 degrees at that depth; the 20,000 pounds of pressure per square inch is enough to crush a dump truck. Even with million-dollar, hard-as-diamond bits, drilling four and five miles through mud, salt, and several layers of rock is painstaking work. In shallower waters, companies could drill 100 or 200 feet an hour, but in the deep water, they're lucky to do that much in a day. Like getting a hit in baseball, in deepwater drilling anything more than a 30 percent success rate is considered excellent.

On Tahiti, the oil comes roaring up from six different wells at a scorching 160 degrees. After it's cooled by seawater, it gets separated from natural gas, pressurized, treated, sold to refineries, and piped back to shore. Twice a day, production-operations manager Tim Bracey pulls a sample from a test line. "That's what we're all out here for," he says, holding up a test tube. "Get this out of the ground, sell it, and make money for the company."

Environmentalists see a slightly more complicated picture. Even when everything goes perfectly, extracting oil from this far underground takes a toll on the environment. "You're going to have spills," says Felicia Marcus, Western director of the Natural Resources Defense Council. "Marine life and coastal communities will be impacted, [so] we have to start asking ourselves if it's worth it."

For Chevron, the answer is obviously yes: next year a handful of new deepwater projects are scheduled to come online. Chevron and its competitors are even working on "ultra-deepwater" projects to extract oil from more than 7,000 feet of water and some 40,000 feet of earth. Someday there may be greener and easier ways to power America. But for now, the conservative cry of "drill, baby, drill" will echo even farther offshore.

With Mac Margolis

© 2010 Newsweek, Inc.

Read more... Sphere: Related ContentOur energy supply: some basics

If a person were to listen to Energy Secretary Steven Chu or National Geographic's Aftermath: World Without Oil, one might think that our energy problems are fairly minor and distant. We can easily add sufficiently renewable energy to substitute for fossil fuels in a fairly short time frame. All we need to do is put our minds (and pocketbooks) to it

by Gail Tverberg | Oil Drum in Energy Bulletin | Mar 12 2010

But if one looks at the situation more closely, one discovers that the situation is quite different. Our energy problems are close at hand, and solutions using what are optimistically called "renewables" are distant and may very well sink the country further into recession.

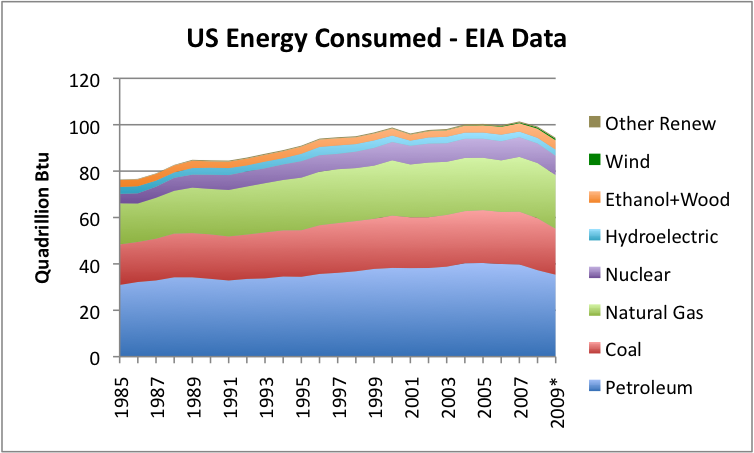

Figure 1- US energy consumption by source, based Energy Information Administration (EIA) Monthly Energy Review Table 1.3. *Year 2009 estimated based on data through November.

US energy consumption is already down quite a bit--some might say due to recession, but it seems even more likely that the result is the other way around--high energy prices squeezed the financial system. This in turn caused credit availability to drop and demand for oil, gas, and coal to drop. We have put a huge amount of effort and subsidies into wind and solar, but they hardly show up on the chart. Ethanol isn't shown separately in the chart this data was taken from--instead it is combined with wood and with other biofuels in a category called "biomass" in the EIA data. The biomass line has thickened a bit, but it is still pretty insignificant.

The following are a few observations about our current situation:

1. Even though wind, solar photovoltaic (PV), geothermal, and ethanol are called "renewables", they cannot be produced without fossil fuels, and need fossil fuels for maintenance.

In many ways, these energy sources should be called "fossil fuel extenders" rather than renewables, because they are very dependent on our current system. For example, growing corn for ethanol depends on tractors run by diesel for growing the corn, and natural gas or coal to power the ethanol plant. Corn is fertilized using fertilizers which are often imported, and sprayed with oil-based insecticides. Wind turbines require regular maintenance, and need to be part of an operating electrical system with fossil fuel back-ups. Solar PV will continue to make electricity once they have been made, but will not produce round-the-clock electricity unless they are part of an electrical system (which requires fossil fuels) or have battery backups which are replaced every few years (also requiring fossil fuels).

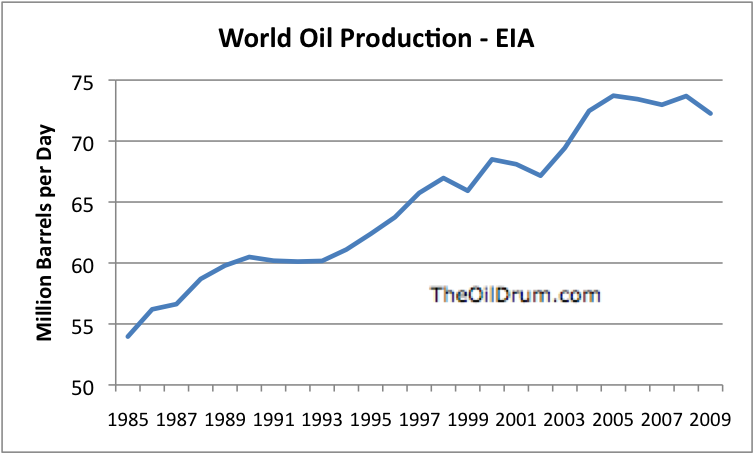

2. World oil production appears to have peaked. If it has not reached its maximum level, its maximum level is likely only a few years away.

Figure 2. World oil production ("Crude and Condensate) from EIA Table 4.1d from International Petroleum Monthly.

World oil production was increasing quite rapidly through 2004 (except for slowing down during recessions). In 2005, the rate of increase dropped, and production has been on a bumpy plateau since--although 2009 appears to be possibly headed downward--or at most on a continuing plateau for a while, before heading downward. There is no longer oil to be found which can be produced inexpensively--most of it was found long ago, and has already been pumped.

Newer sources of oil tend to be more expensive. If economies could really afford $200 or $300 or $400 barrel oil, and had unlimited capital, perhaps production could increase some more. But at some point, we run short of capital for more and more expensive new production, and the high price of oil tips the economy into recession and dampens demand.

Many analyses are reaching the same conclusion about world oil production. Just this week, a new studyfrom Kuwait predicted oil production may reach a peak and decline in 2014. The International Energy Agency has also been talking about the possibility of a peak before 2020.

3. Whether the peak in production is from Peak Supply or Peak Demand, the result for the consumer is equally bad--recession, reduced job availability, and increasing loan defaults.

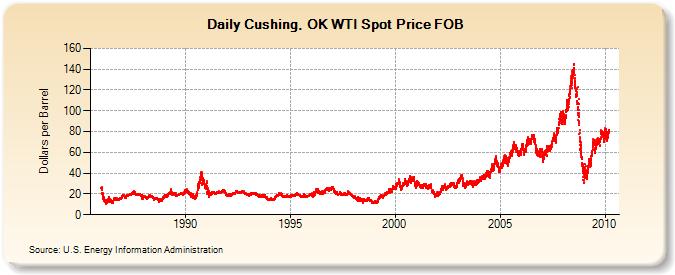

It does not really matter whether one puts the label "supply constraint" or "demand constraint" on the resulting drop in production--the effect is the same. Prices are still high relative to historical prices, even through the world is struggling to emerge from recession, as shown in Figure 3 below.

Figure 3. Spot oil prices for benchmark West Texas Intermediate. Graph by EIA.

Oil is essential for food production and transportation. Consumers tend to cut back on discretionary purchases (causing recession) or to default on their loans, if their budgets are squeezed by high prices oil prices. James Hamilton was one economist showing a link between high oil prices and recession.

4. Scaling up renewables to replace fossil fuels in current quantities does not look like it has much of a chance of succeeding, even in the long term.

One issue is the point made previously--it takes fossil fuels to produce renewables like wind and solar PV. Also, Figure 1 shows our success in scaling up so far has been quite limited. Scaling up ethanol further would require taking a huge share of our corn crop. Cellulosic ethanol isn't working out to date, and may never work out. Wood and other biomass is limited in supply, limiting production if it could be perfected.

There may be some particular applications of renewables which may turn out to work out well--for example, natural gas from waste, or biofuel from waste grease. But these tend to be limited in quantity.

Even if we were to, say, discover a way of producing biofuel from algae economically, it would years to work out the details of scaling production up, and a huge amount of investment (and fossil fuels to make tanks and other apparatus) to actually produce the biofuel in quantity. One would probably be looking at more than 30 years before the process could be scaled up sufficiently to start replacing a significant share of our our production.

5. Natural gas will not solve all of our problems.

There has been considerable publicity about the US having "100 years of natural gas" available at current usage levels. There are several issues, however:

a. Natural gas will not run in our current vehicles. Fixing vehicles to run on natural gas, and adding infrastructure to deliver the gas, is likely to be expensive and take quite a few years.

b. If we were to use natural gas for transportation, supply would run out very quickly--perhaps 20 years or use, or even less. Look at natural gas use, compared to oil use on Figure 1.

c. It is not clear that the "100 years of natural gas" is available at prices consumers can afford. If the price is high, we may very well have the same "peak demand" issue we have for oil--people will not be able to afford huge electric bills and huge home heating bills--say double today's level.

d. Scaling up natural gas faces huge challenges. Our infrastructure is only built for the current usage of natural gas. Adding more pipes, storage, and end usage is very expensive and time consuming. If the timing of the new infrastructure is slower than the increase in gas production, gas prices are likely to plunge or stay too low for profitability.

e. There are concerns regarding "fracking" near major water supplies, such as that of New York City. Expansion of natural gas may not occur to the extent that many are hoping will take place in the 100 year supply numbers.

6. If increased drilling is done in the US and offshore, is likely to have modest beneficial impact on oil supply, but it is highly unlikely that it will solve our problems.

Gary Luquette, President of Chevron North America Exploration and Production recently wrote:

The good news: the OCS [Outer Continental Shelf] has significant potential. Over time, it could add 1 million more barrels of oil and natural gas equivalent a day--potentially representing a fifth of the current total U.S. oil production. Advances in technology could increase that amount dramatically.

One million barrels of oil and natural gas equivalent is great--certainly more than what we are getting from biofuels or from wind or solar. If one adds additional onshore production, it could be more than this, perhaps another 1 or even 2 million barrels of oil and natural gas equivalent a day.

But remember, this isn't even all oil--part of this is natural gas, the problems of which were described in Item 5, above. Compared to the world's oil supply, an additional one million barrels of oil a day about 1% of world oil production. Compared to US oil usage, an additional one million barrels of oil a day is about 5%. So the additional oil supply would be helpful, (as would the additional jobs, and reduction in needed imports), but it wouldn't solve all of our problems.

Also, if the price of the new oil supplies turns out to be too expensive (because, for example, the cost of drilling in deep water is too expensive), we may find that the new supplies are really more expensive than the economy can afford. Oil prices may remain below the cost of production, bringing a fairly quick end to new production--oil companies will soon quit production, if deep sea (or other new production) is clearly a money loser.

7. Renewables tend to be high priced. If our big problem with oil is high price, renewables will not solve our problems.

Subsidies only hide high price--the cost to the economy is high, with or without a subsidy.

If we can find cheap renewables, it would be in our interested to expand them as much as possible. But expanding expensive renewables should be done with great caution, in my opinion. We have no guarantee regarding how long the renewables will last--wind is likely only to last as long as fossil fuels supplies are available. Just because an analysis is done assuming that wind (or another energy source) will have a 40 year lifetime doesn't mean it will actually last that long.

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Read more... Sphere: Related Content13 March 2010

An unconventional glut

Newly economic, widely distributed sources are shifting the balance of power in the world’s gas markets

The Economist | Mar 11th 2010

SOME time in 2014 natural gas will be condensed into liquid and loaded onto a tanker docked in Kitimat, on Canada’s Pacific coast, about 650km (400 miles) north-west of Vancouver. The ship will probably take its cargo to Asia. This proposed liquefied natural gas (LNG) plant, to be built by Apache Corporation, an American energy company, will not be North America’s first. Gas has been shipped from Alaska to Japan since 1969. But if it makes it past the planning stages, Kitimat LNG will be one of the continent’s most significant energy developments in decades.

Five years ago Kitimat was intended to be a point of import, not export, one of many terminals that would dot the coast of North America. There was good economic sense behind the rush. Local production of natural gas was waning, prices were surging and an energy-hungry America was worried about the lights going out.

Now North America has an unforeseen surfeit of natural gas. The United States’ purchases of LNG have dwindled. It has enough gas under its soil to inspire dreams of self-sufficiency. Other parts of the world may also be sitting on lots of gas. Those in the vanguard of this global gas revolution say it will transform the battle against carbon, threaten coal’s domination of electricity generation and, by dramatically reducing the power of exporters of oil and conventional gas, turn the geopolitics of energy on its head.

Deep in the heart of Texas

The source of America’s transformation lies in the Barnett Shale, an underground geological structure near Fort Worth, Texas. It was there that a small firm of wildcat drillers, Mitchell Energy, pioneered the application of two oilfield techniques, hydraulic fracturing (“fracing”, pronounced “fracking”) and horizontal drilling, to release natural gas trapped in hardy shale-rock formations. Fracing involves blasting a cocktail of chemicals and other materials into the rock to shatter it into thousands of pieces, creating cracks that allow the gas to seep to the well for extraction. A “proppant”, such as sand, stops the gas from escaping. Horizontal drilling allows the drill bit to penetrate the earth vertically before moving sideways for hundreds or thousands of metres.

These techniques have unlocked vast tracts of gas-bearing shale in America (see map). Geologists had always known of it, and Mitchell had been working on exploiting it since the early 1990s. But only as prices surged in recent years did such drilling become commercially viable. Since then, economies of scale and improvements in techniques have halved the production costs of shale gas, making it cheaper even than some conventional sources.

The Barnett Shale alone accounts for 7% of American gas supplies. Shale and other reservoirs once considered unexploitable (coal-bed methane and “tight gas”) now meet half the country’s demand. New shale prospects are sprinkled across North America, from Texas to British Columbia. One authority says supplies will last 100 years; many think that is conservative. In 2008 Russia was the world’s biggest gas producer (see chart 1); last year, with output of more than 600 billion cubic metres, America probably overhauled it. North American gas prices have slumped from more than $13 per million British thermal units in mid-2008 to less than $5. The “unconventional”—tricky and expensive, in the language of the oil industry—has become conventional.

The availability of abundant reserves in North America contrasts with the narrowing of Western firms’ oil opportunities elsewhere in recent years. Politics was largely to blame, as surging commodity prices emboldened resource-rich countries such as Russia and Venezuela to restrict foreign access to their hydrocarbons. “Everyone would like to find more oil,” says Richard Herbert, an executive at Talisman Energy, a Canadian firm using a conventional North Sea oil business to finance heavy investment in North American shale. “The problem is, where do you go? It’s either in deep water or in countries that aren’t accessible.” This is forcing big oil companies to get gassier.

The oil majors watched from the sidelines as more entrepreneurial drillers proved shale’s viability. Now they want to join in. In December Exxon Mobil paid $41 billion for XTO, a “pure-play” gas firm with a large shale business. BP, Statoil, Total and others are sniffing around the North American gas patch, signing joint ventures with producers such as Chesapeake Energy. A wave of consolidation is likely in the coming months, as gas prices remain low, the drillers seek capital and the majors hunt for the choicest acreage.

Shale is almost ubiquitous, so in theory North America’s success can be repeated elsewhere. How plentiful unconventional resources might be in other regions, however, is far from established. The International Energy Agency (IEA) estimates the global total to be 921 trillion cubic metres (see chart 2), more than five times proven conventional reserves. Some think there is far more. No one will really know until companies explore and drill.

The drillers are already arriving in Europe and China, which are both expected to import increasing amounts of gas—and are therefore keen to produce their own. China has set its companies a target of producing 30 billion cubic metres a year from shale, equivalent to almost half the country’s demand in 2008. Several foreign firms, including Shell, are already scouring Chinese shales. After a meeting between the American and Chinese presidents last November, the White House announced a “US-China shale gas initiative”: American knowledge in exchange for investment opportunities. The IEA says China and India could have “large” reserves, far greater than the conventional resource.

Exploration is also under way in Austria, Germany, Hungary, Poland and other European countries. The oil industry’s minnows led this scramble, but now the big firms are arriving too. Austria’s OMV is working on a promising basin near Vienna. Exxon Mobil is drilling in Germany. Talisman recently signed a deal to explore for shale in Poland. ConocoPhillips is already there. The first results from wells being drilled in Poland, in what some analysts believe is a shale formation similar to Barnett, should be released this year.

No one expects production of shale gas in Europe to make a material difference to the continent’s supply for at least a decade. But the explorers in China and Europe present a long-term worry for those who have bet on exporting to these markets. Gazprom, Russia’s gas giant, is the company most exposed to this threat, because its strategy relies on developing large—and costly—gasfields in inhospitable places. But Australia, Qatar and other exporters also face a shift in the basics of their business.

Choked

These producers are already getting a taste of the global gas glut. Almost in tandem with the surge in American production, recession brought a slump in world demand. The IEA says consumption in 2009 fell by 3%. In Europe, the drop was 7%. Consumption in the European Union will grow marginally if at all this year and will not be sufficient to clear an overhang of supplies, contracted through take-or-pay agreements signed in the dash for gas of the past decade. IHS Global Insight, a consultancy, reckons that the excess could amount to 110 billion cubic metres this year, almost a quarter of the EU’s demand in 2008.

The glut has been exacerbated by the suddenly greater availability of LNG. Importers with the infrastructure to receive and regasify LNG can now easily tap the global market for spot cargoes. This is partly a product of the recession, which dampened demand from Japan and South Korea, the leading LNG buyers. But another cause is that many exporters, not least Qatar, the world’s LNG powerhouse, spent the past decade ramping up supplies aimed at the American market. That now looks like a blunder.

America is still taking some of this LNG, but the exporters’ bonanza is over before it ever really began. “You’ll always find a buyer in North America,” says Frank Harris, an analyst at Wood Mackenzie, a consultancy, “but you might not like the price.” And LNG will grow increasingly abundant as new projects due to come on stream this year add another 80m tonnes to annual supply, almost 50% more than in 2008.

Gas out, money in

Qatar’s low production costs mean it can still make money, even in North America. Others cannot. In February, for example, Gazprom postponed its Shtokman gasfield project by three years because of the change in the market. Some of the gas from that field, in the Barents Sea, was to be exported to America. But Shtokman’s gas will be costly, because the field is complex and its location makes it one of the world’s most difficult energy projects to execute. Some analysts now wonder whether gas will ever flow from Shtokman.

China offers some hope for ambitious exporters, but even there the outlook has become cloudier. The Chinese authorities want natural gas to account for at least 10% of the country’s energy mix by 2020 and are building LNG import terminals. With that target in mind, Australia, which has its own burgeoning conventional and unconventional gas supplies, has been busily building an LNG export business. But warning lights are coming on. In January, PetroChina let a deal to buy gas from Australia’s Browse LNG project expire. The original agreement was made in 2007, when LNG prices were soaring in Asia, but China can afford to be picky now. “Too many Australian LNG plants are chasing too little demand,” says Mr Harris.

The shift in the global market has left China well-placed to dictate prices. This will be another blow to Gazprom, which has long talked of exporting gas to the country. Indeed, while the Chinese and the Russians have squabbled over the terms, Turkmenistan has quietly built its own export route to China. Even if Beijing’s shale-gas plans come to nothing, supplies from Central Asia and new regasification terminals along its coast may allow China to reach its natural-gas consumption targets without pricey Siberian supplies.

The glut has weakened Gazprom’s position in Europe, too. It has been losing market share to cheaper Norwegian and spot-market supplies. In 2007 Gazprom talked of increasing its annual exports to the EU to 250 billion cubic metres. Now, says Jonathan Stern, of the Oxford Institute for Energy Studies, Gazprom will probably only ever supply the EU with 200 billion cubic metres a year (it shipped about 130 billion in 2008). The company forecast in 2008 that its gas prices in Europe would triple, to around $1,500 per 1,000 cubic metres, on the back of rising oil prices, which help set prices in long-term contracts. But the price dropped to about $350 last year and is expected to fall again in 2010. The weak market could last for another five years, believes Wood Mackenzie. Gazprom has been renegotiating with leading customers, injecting elements of spot pricing into contracts to make them more attractive.

Shtokman shtymied

Moreover, Europe’s need for new pipelines to guarantee supplies suddenly looks less pressing. Construction of Nord Stream, Gazprom’s flagship project to export gas directly to Germany through the Baltic Sea, will begin next month. It is due to come on stream in 2011. The scheduled doubling of its capacity to 55 billion cubic metres a year is in doubt, says Mr Stern, because Shtokman was to have supplied the gas for it.

Demand is a bigger problem. Even without recession or European shale, the assumption that Europe’s consumption will keep growing is looking shaky, because the EU’s efforts to boost efficiency and reduce carbon emissions are making gradual headway. Edward Christie, an economist at the Vienna Institute for International Economic Studies, says the EU could be importing a third less natural gas in 2030 than the European Commission forecast in 2005. That makes the case for additional supply lines much less compelling. The IEA expects rich European countries’ demand to grow by only 0.8% a year in the next two decades, against 1.5% for the world as a whole (see chart 3).

An age of plenty for gas consumers and of worry for conventional-gas producers thus seems to be dawning. But two factors could reverse the picture again. The first surrounds the uncertainty about how fruitful shale exploration will be outside North America. A clearer understanding of the geology will emerge from pilot wells in the coming months. Second, there are reasons for caution above ground, too. Despite natural gas’s greener credentials than oil’s or coal’s, shale drilling has critics among environmentalists, who worry that water sources will be poisoned and landscapes despoiled.

The industry says cement casing of wells and the depth to which they are drilled make the practice safe and relatively unobtrusive. But so far it has been drilling mainly in North America, where land is plentiful and people are accustomed to the sight of oilmen’s detritus. In densely populated Europe, the rapacious rate at which shale plays must be drilled to sustain production is less likely to be tolerated.

Even in America, opposition to shale gas is rising. New York state has imposed a moratorium on drilling in its portion of the Marcellus Shale, which it shares with Pennsylvania. Lawmakers in Congress want to study the ecological impact of fracing. The Environmental Protection Agency, a federal body, also raised concerns about “potential risks” to the watershed.

The path of demand in gas’s new age is hard to predict, but abundant new sources could bring about profound change in patterns of energy consumption. Some of the downward pressure on price will ease: despite sedate growth, the LNG glut should dissipate, probably by 2014, says Mr Harris; and low prices will kill more projects, clearing the inventory. France’s Total thinks global demand will recover strongly enough to require another 100m tonnes a year of LNG by 2020, on top of plants already planned. However, the Energy Information Administration, the statistical arm of America’s Department of Energy, predicts decades of relatively weak prices.

If this is correct, it makes sense, for both environmental and economic reasons, for the country to gasify its power generation, half of which comes from coal-fired plants. This could be done cheaply and quickly, because America’s total gas-fired capacity (as opposed to production) already exceeds that for coal. Put a price of only $30 a tonne on carbon, say supporters, and natural gas would quickly displace coal, because gas-fired power stations emit about half as much carbon as the cleanest coal plants. The IEA agrees that penalising carbon emissions would benefit natural gas at the expense of dirtier fuels.

There would be political obstacles. The coal lobby remains strong in Washington, DC. Climate legislation struggling through Congress even includes provisions to protect “clean coal”, a term covering an array of measures, so far uncommercial, to reduce emissions from burning the black stuff. Ironically, oil companies that were once suspicious of proposals to control carbon now regard a carbon price or even a carbon tax as a potential boon to their new gas businesses.

A more radical idea, and one that would have ramifications for the global oil sector, is to gasify transport. T. Boone Pickens, a corporate raider turned energy speculator, has launched a campaign to promote this, and has support from the gas industry. By converting North America’s fleet of 18-wheeled trucks to natural gas, says Randy Eresman, boss of EnCana, a Canadian gas company, America could halve its imports of Middle Eastern oil. EnCana is promoting “natural gas transportation corridors”: highways served by filling stations offering natural gas.

All this is some way off. The coal industry will not surrender the power sector without a fight. The gasification of transport, if it happens, could also take a less direct form, with cars fuelled by electricity generated from gas.

A gasified American economy would have profound effects on both international politics and the battle against climate change. Displacement of oil by natural gas would strengthen a trend away from crude in rich countries, where the IEA believes demand has already peaked as a result of the recent spike in oil prices. Another consequence of the energy market’s bull run, the unearthing of vast new supplies of gas, could bring further upheaval. If the past decade was characterised by the energy-security concerns of consumers, the coming years could give even the world’s powerful oil producers reason to worry, as a subterranean revolution shifts the geopolitics of global energy supply again.

Copyright © The Economist Newspaper Limited 2010. All rights reserved.

Read more... Sphere: Related Content12 March 2010

Drought ravages famed Philippine rice terraces

A worsening drought is exacting a terrible toll on the world-famous mountain rice terraces of the northern Philippines, local officials said Tuesday

AFP in Yahoo! News | Mar 9, 2010

AFP/File – A farmer (bottom L) plants rice in a paddy field in the scenic Banaue rice terraces in the northern mountainous …

A state of calamity was this week declared for the Banaue area that is home to many of the ancient stone-walled paddies and one of theSoutheast Asian nation's most popular tourist destinations, the officials said.

"The tourists still come here, but all they see are parched fields andforest fires and leave disappointed," Abriol Chuliba, chief aide to the Banaue mayor, told AFP in a telephone interview.

The rice terraces, a United Nations World Heritage site and known locally as the "Eighth Wonder of the World", were built between 2,000 and 6,000 years ago using huge rocks for each step and a complex trickle-down irrigation system.

Banaue tourist information bureau officer Juliet Mateo said the rice paddies most frequented by tourists at Batad and Bangaan had dried up completely as much of the country suffered from an El Nino-induced drought.

Mateo said the rice harvest, which takes six months in the mountains compared with three months on the flats, was in danger of being ruined completely by the drought.

"The mountain rice was planted in December and January, but the way things are going there won't be anything left to harvest in June and July," Mateo told AFP.

She said Ifugao province governor Teodoro Baguilat had declared the state of calamity for Banaue on Monday. This allowed local authorities to tap into emergency funds to help farmers.

Chuliba said seasonal rains ceased completely last month, causing the mountain springs upstream of Batad and Bangaan that water the terraces to dry up.

"Not all areas are affected, but if this will continue until next month they won't be able to plant anything anymore," he said of the other terraces in Ifugao.

He said it was the worst dry spell he could remember in the area since another El Nino-induced drought in 1998.

The national government has said the drought, caused by cyclical warming of the waters of the Pacific Ocean, is set to last until the middle of the year.

The government expects the rice output of the Philippines, already the world's top rice importer, to decline further due to drought, forcing it to ship in more of the staple grain from abroad.

However the Ifugao rice terraces, which cover an area of 22,000 hectares (53,000 acres), are more important to the country as a tourism attraction than a source of rice.

Copyright © 2010 Agence France Presse. All rights reserved

Copyright © 2010 Yahoo! Inc. All rights reserved

Read more... Sphere: Related Content07 March 2010

Expert: Australia like drug dealer of coal

A climate scientist often referred to as the "godfather of climate change" said Australia's massive coal exports are almost equivalent to being a drug dealer to the world

United Press International | March. 4, 2010

Dr. James E. Hansen, director of the NASA Goddard Institute for Space Studies, speaks at National Press Club to mark the 20th anniversary of the "Hansen Hearing," the Senate Energy Committee's 1988 hearing on climate change, which marked the first time a top climate scientist declared that global temperatures had risen beyond the range of natural variability in Washington on June 23, 2008. (UPI Photo/Patrick D. McDermott)

In kicking off his visit to Australia for a series of lectures on nuclear energy, James Hansen, director of NASA's Goddard Institute for Space Studies, had a message for the world's largest exporter of coal: Phase it out.

Australia exported about 60 percent of its coal production in 2008 -- about 268.5 million tons -- accounting for 25 percent of global coal exports.

Hansen said pollution from fossil fuels was killing 1 million people a year and that the planet was doomed if emissions were not dealt with, The Age reports.

Coal-fired power stations, known for high carbon dioxide emissions, generate about 80 percent of Australia's electricity.

Nuclear power, Hansen said, is an inevitable part of the solution for climate change.

"Renewable energy and nuclear power together can solve the air and water problem, as well as the climate problem,'' he said.

Hansen noted that he would be open to Australia making a commitment to move to 100 percent renewable energy but renewable sources cannot be relied on alone. It becomes a choice between coal and nuclear for base-load power, he said.

But while a Nielsen poll last October indicated 49 percent of Australians support nuclear energy, Australian Prime Minister Kevin Rudd has rejected the prospect of nuclear power for his country, saying last month that coal's importance will remain "huge" until 2050.

Touching on the Australian government's embattled emissions trading scheme regarded by Rudd as the best way to tackle climate change, Hansen said it was a "non-solution."

The Australian Senate rejected ETS legislation in December for a second time. Further debate on the legislation is postponed until May.

Hansen said he supported the Green Party's plan for an interim carbon tax starting at $23 a ton for two years while agreement was reached on the best type of carbon pricing. He noted that this "Plan B" is in line with his support of industries having to pay a carbon price without access to offsets through a carbon market.

''If we had a democracy where decisions were based on the public's best interest, then that would be taken up in a heartbeat," Hansen said, the Sydney Morning Herald reports. But "neither of the major parties gets it -- or they don't want to get it.''

As for Australia's opposition party, Hansen said it has not accepted the idea of man-made climate change.

''I don't intend to be telling Australia what they should do for their energy source except that they can't continue to burn coal without screwing everybody -- including my grandchildren," he said.

Hansen's book, "Storms of My Grandchildren: The Truth About the Coming Climate Catastrophe and Our Last Chance to Save Humanity," was published in December.

© 2010 United Press International, Inc. All Rights Reserved

Read more... Sphere: Related Content24 February 2010

Uganda: Floods Paralyse Business

On Monday, business was paralysed after hours of rain in Kampala and some other parts of the country

Zaharah Abigaba | The Monitor in AllAfrica.com | 23 February 2010

The rains that started at around 4am stretched up 5pm, making it hard for city dwellers to report to work on time and hundreds of students were left stranded.

Floods left several people stranded in the flood prone areas of Kawempe, Bwaise, Katwe, Kalerwe and Bugolobi.

Most schools in Bukasa and Kamalimali zones of Kalerwe registered a low turn up, partly because the children could not wade through the flooded roads.

Many areas in Salaama- Munyonyo were flooded too.

Most shops remained closed and in the usually busy down-town Kampala businesses remained closed the whole day.

In Kanungu, a severe hailstorm on Sunday swept through the district, destroying the district administration council hall, following a heavy downpour that lasted almost two hours.

Ms Josephine Kasya, the Kanungu LC5 chairperson said more than seven tonnes of chicken mash supplied to the district by the National Agricultural Advisory Services programme were destroyed.

In Jinja, rain paralysed business and in Gulu, it drizzled from morning till 4pm.

According to the Department of Meteorology, rains are expected to continue up to May "but they will not be disastrous."

"The ongoing rains are expected to continue up to May and we shall give a detailed forecast about the rains next week that will reflect other regions of the country," said Mr Jackson Rwakishaija, the senior communications officer at the Meteorology Department.

According to the weather forecast for January and February released by the department last month parts of Lake Victoria Basin, Central, South Eastern, and South Western regions were expected to continue receiving rainfall (normal to above normal rains) as the ongoing El-Nino continues into the first quarter of 2010.

Copyright © 2010 The Monitor. All rights reserved

Read more... Sphere: Related Content23 February 2010

Sustainability, lasting recovery, and other myths

For the world economy to be considered sustainable; that is, to reach and maintain a decent level of living for the entire global population for a century or two, the use of renewable resources should not exceed sustainable yields; pollution levels should not surpass the environment’s absorbing/regenerating capacity; the drawdown of nonrenewable resources should decline in proportion with the depletion of stocks; and environmental goals and technical progress helping to achieve them ought to gain universal application

by Peter Pogany | Energy Bulletin | Feb 22 2010

Even minimum acquaintance with data and trends is sufficient to recognize that the world is running away from any feasible configuration of sustainable balance among the critical variables of population levels, environmental impact, and resource demand.

Projections -- a mishmash of the good, the bad, and the impossible

Waxing GDP to the max remains the international community’s central economic objective. Pedal to the metal -- there is no speed limit on the turnpike to Canaan!

At the 3.0 - 4.0 percent annual clip, widely used in official forecasts, the world should see an expansion in its output anywhere from 86 percent to more than double its current level by 2030. This dazzling prospect of making everybody richer and reducing, if not eliminating, abject poverty and hunger is often juxtaposed with the good news that global population growth is on track to decelerate, from a 29 percent during 1990-2010, to 20 percent during 2010-2030.

The appearance of more than one billion people by 2030 is being largely attributed to a “youth-bulge-driven momentum,” the rise of reproduction age cohorts relative to the total population. As replacement-level fertility stabilizes the human biomass, a shift of mind toward reproduction, labeled “demographic transition,” is expected to take place in the lower registers of the income scale. The poor are poor alright but, thanks to economic growth, less and less so, and once a certain level of material well-being is reached, they will want to improve the quality of their progenies’ life through care and education rather than just increasing their number. “Demographic transition” has indeed been observed in the rich countries.

But prospects are much less rosy when we look at absolute numbers. Planetary occupancy could easily reach 10 billion by mid-century, roughly three billion more than now -- as increase as big as the entire world population at the time JFK took office in 1960.

Several first-rate academic investigations show that generalizing developed country living standards (enjoyed by one-fifth of the world population) even for the current ca. 6.8 billion people is impossible without provoking severe resource shortages and ruining the environment beyond repair. Making the same calculations with ten billions yields a tragic incongruity -- the name MALTHUS keeps flashing on the computer screen.

Arguments that “demographic transition” will be accompanied by “economic transition” toward services and a nonresource-intensive knowledge economy are flatly wrong.

They are based on the limited experience of the most developed countries where “economic transition” has been made possible by importing resource-intensive and polluting manufactures from the rest of the world.

Reaching the enormous fixed cost that comes with successful industrialization presupposes major increases in the throughput of material resources. Real estate services, web page design, marriage counseling, and consultancy on interior decoration are no substitutes for metals, minerals, timber, and energy carriers needed to build and equip developed-country-standard homes for billions of slum dwellers. And once the fixed cost associated with high development is in place, it requires maintenance; a continued throughput with polluting side effects.

Given that physical and economic considerations properly order units of natural wealth according to ease of access and cost of extraction, the throughput will be increasingly expensive. One way or another, this process will check the combined thrust of demographic and economic expansion.

In our era, the world behaves like a young tree, fully confident that it will continue to grow forever. How could its miraculous system of accelerated cell accumulation ever fail to widen the trunk, thicken the branches, and push the twigs to divide and multiply? In the same way that nature does not allow trees to become skyscrapers, it also has its own foolproof ways of breaking the momentum towards turning the planet into an ever larger shopping mall, with ample parking for billions and billions of old and new, increasingly affluent customers.

Inconsistencies in long-term energy projections

The hybrid of encouragement and discouragement found in overall growth forecasts is reproduced when looking at energy.

Remaining heavily dependent on fossil fuels is the only way to realize the envisaged growth. A disturbing consequence is that carbon dioxide emissions during the forecast period (2010-2030) are expected to match the increase during the previous two decades. This is a clear disaster in terms of climate change, biodiversity, and water supply. It conjures up the chilling specter of losing the last opportunity to bring environmental degradation under voluntary control.

Oil consumption is supposed to increase from ca. 86 million barrels per day (mb/d) in 2008 to 105 mb/d in 2030. (Source: International Energy Agency, IEA, World Energy Outlook. Assessments made by the U.S. Energy Information Administration, EIA, match these figures.)

Independent oil industry experts have serious doubts that this need-based prospect will ever be fulfilled. And if push comes to shove in substituting the less polluting and more abundant natural gas for oil, its reservoir would undergo exponential diminution, putting the problem of an overbuilt, economically unviable delivery infrastructure on the back of the next generation.

Ignoring the overall picture portends colossal consequences.

Energy intensity (global energy demand per aggregate global output), which declined during the 20th century as well as during the past decade, is projected to stay on a diminishing path. The growth factor of world output at constant prices will exceed that of aggregate energy use. Unecological economics sees reason to celebrate. “Efficiency” is its magic word, pronounced as if it should be accompanied by the sound of sacred clarions. Taken by its narrow definition, it is far from being an unqualified blessing in the present context.

While the productivity of energy carriers is supposed to increase (reducing their relative costs), total energy demand is on the uptick. Based on the latest EIA projections (reference case) and historical data, increase in per capita worldwide energy consumption should accelerate to 18 percent during 2010-2030, from an estimated less than 10 percent during the previous 20 year period (1989-2009).

Our civilization is predominantly nonrenewable resource-based and there is no responsibly anticipatable technology to change that. No matter how one nonrenewable is substituted for another, global economic expansion has been made possible and will remain contingent on increasing the scale of returns on the planet’s fixed supply of once-in-a-geological epoch reservoir of energy carriers and other substances, accelerating its depletion.

Where exponential positive growth (i.e., in world GDP) nourished by exponential negative growth in the planet’s exhaustible resources leads should be obvious.

If we suspend our Zeitgeist-hardened faith in the free-floating myths of unlimited technological perfectibility and the aptness of private profit-driven, decentralized decision-making to solve any and all resource and environmental problems rationally and just in time, the judgment seat of reality hands out a stark verdict. The world will either grow as scheduled and poison itself in the process or it will lose its growth crusade while breathing only moderately harmful air.

The intellectual and moral task of our generation is to recognize this.

Convincing transition to renewable energy in our lifetime! Myth or reality?

The jury is still out.

Caution when examining anything heretofore unseen, and respect for those who work with enthusiasm to accomplish the transition demand that this be said.

Yes, but not much longer.

While forecasts show significant expansion in practically all subsectors of renewable energy (solar, wind, hydro-, bio- and geothermal sources) their combined ratio barely budges. Overall growth in the worldwide demand for joules is to blame. EIA data indicate that renewable energy’s share in global electricity generation (the primary use of renewables) is expected to reach 21 percent by 2030, too close to the recorded 19 percent in 2006 to consider it a major advance toward laying the foundations of sustainability.

The hope is that several national programs that go beyond average worldwide forecasts will make a difference.

For example, the current U.S. Administration has set the goal of increasing renewable sources in electricity generation from their actual ca. 10 percent to 25 percent in 15 years. This would indeed be a vital step toward ecological sustainability in the United States, but it is a tall order: Private investment in the development of nonhydropower sources, which are counted on to accomplish the bulk of the structural shift, remains sluggish and unpredictable.

Independent of economic conjuncture, irrationality arches over the whole idea of wanting to implement a drastic resource transition under the banner of sustainability while trying to maximize output. Preference for growth through “full employment now” policies prevails and so does the inertia of remaining dependent on fossil fuels.

To the extent and the manner in which the “25 percent by 2025” objective is or is not fulfilled, American society will learn a great deal about the viability of government and business relations in the mixed economy. At the slightest falter, questions about the distribution of responsibilities will surface.

It all boils down to the basic question: “How do we recognize that growth is being constrained?”

There is no easy answer. Without irrefutable proof, the theoretical impossibility of everlasting exponential economic expansion in our thermodynamically closed sphere cannot be fully comprehended.

Evidently, only a general economic reversal or some environmental calamity would qualify. Analytical work citing tables and charts do not rise to the same level because they can always be effectively opposed by other tables, charts, and expert opinion. But this feature of the collective learning process should not prevent us from continuing to argue that “business as usual” economic growth has come to an end.

The oil constraint showed up in a definitive way during the same decade when the danger of ecological degradation became acute and world finances reached a critical point. Unfortunately, a synthesis-disabling pecking order among the three symptoms prevents their unification into a single, influential observation.

In most analyses dealing with “limits to economic growth,” natural resource problems (“peak oil” in the lead) take precedence over the environment. The financial dimension is considered wholly unrelated. Since the sheer possibility that a specific matter may constrain growth is a black hole in the firmament of contemporary economic understanding, the nexus will remain undiscovered for some time.

Yet it can hardly be mere happenstance that arrangements and routines in the world’s dollar-based monetary order, which had survived recessions, politically-motivated oil shortages (“1973” and “1979”), financial crises, privately-engineered speculative tricks and covertly pursued, system-harming national strategies for over half a century, would fall into disorder during the decade when growth in the demand for the world’s pivotal material resource (conventional oil) went unanswered by increased supplies.

The price of the globally narrow resource constraint rising to a level where it endangered the profitability of production in general was the slip that caused the surreal pile of over-extended and over-specialized payment obligations to start tumbling. The emphasis is on “start.”

“You Ain't Seen Nothing Yet!” (Indeed)

Oil is the dominant underlying natural substance in any valid structural representation of the world economy.

Coupling this certainty with the proposition that we have unwittingly passed the peak (or “a” peak, at least) in its planet-wide production with demonstrated inability to substitute away from it while preserving growth, one may begin suspect a gross misunderstanding.

While the ensemble of oil producers is regarded as capable of moving along an upward sloping long-run supply curve (i.e., by bringing more costly conventional and non-conventional reserves into use), output and investment data combined with available information about reserves suggest otherwise. None of the producers will ever deliver more at the same price. That is, the supply curve of this patently increasing-cost industry cannot shift in the expected direction. Elementary microeconomics helps visualize the logical bond between an upward sloping long-run supply curve and interim shifts in shorter-run marginal cost schedules.

“Here’s looking at you . . . abundant energy at noncrippling prices.”

The gap between expectations and reality appears to have created an unsavory servo-mechanical feedback circuit.

WFEP, worldwide factor elasticity of production (output response to a unit increase in all the resources combined), which is crucially dependent on abundant oil supplies, is stuck between zero and some relatively low positive number. At zero (disrupted growth reduced prohibitive oil prices to affordable levels), a process would turn the global economy toward that positive number, which, when approached, would lead to an increase in oil prices, sending WFEP back toward zero.